- READ MORE: The average U.S. credit score DROPS for the first time in ten years

Credit scores are a crucial aspect of overall financial well-being.

However, these scores — which determine our eligibility for crucial financial services like mortgages, auto loans, and credit cards — are similarly marred by inaccuracies.

Credit scores range from 300 to 850. Any score below 629 is regarded as 'poor'. Anything over 720 is considered 'excellent'. as stated by the credit scoring firm FICO.

A low score might lead to increased interest rates on loans And even being considered unfit for financial products like mortgages.

Here is financial expert Monique White, who leads the community at Self Financial - This service assists Americans in enhancing their credit scores - debunks the top five credit score misconceptions and provides tips on avoiding them.

1. Reviewing your personal credit report can negatively impact your score.

Understanding your financial position is crucial for achieving monetary success, and reviewing your credit report serves as a means to gain an comprehensive perspective on your economic situation.

A lot of individuals think that reviewing your personal credit report can lower your credit score.

Although you should be wary of credit checks that result in hard inquiries, checking your own report is considered a soft inquiry and does not affect your score.

You can obtain your credit report without charge at annualcreditreport.com.

2. Keeping a balance on your credit card can contribute to improving your score.

Many people think that keeping a low balance on your credit card can assist in building up your score.

Nevertheless, maintaining an outstanding balance on your credit card over multiple months will result in accruing interest charges.

A rule of thumb for revolving debt is to keep your balances below 30 percent of your available credit.

However, it's advisable to settle your entire credit card balance each month to sidestep fees and maintain a low usage rate.

3. You possess just a single credit score.

The three primary credit-reporting agencies are Experian, Equifax, and TransUnion.

Various bureaus might possess distinct information regarding your credit actions (such as accounts and collection records), leading to potential discrepancies in the scores they provide.

Although FICO and VantageScore are the predominant credit scoring models, various iterations and sector-focused credit ratings can lead to differing scores. This variance depends on both the lender and the specific kind of credit you’re seeking.

4. The amount of money you earn influences your credit score.

Even though your income can affect whether you get approved for specific loan products, it does not influence your credit score.

Your score is determined by five elements: your payment history, how much of your available credit you're using, the duration of your credit history, any recent applications for new credit, and the variety of credits you possess.

5. Upon getting married, you will jointly have a single credit score with your partner.

Marriage doesn't merge your credit scores as an automatic process.

Everyone will maintain an individual score that reflects their personal financial background.

If a couple decides to jointly apply for credit cards, co-sign a loan, or add each other as authorized users, this action will affect both of their credit reports.

Therefore, it's crucial to bear this in mind when making joint financial choices.

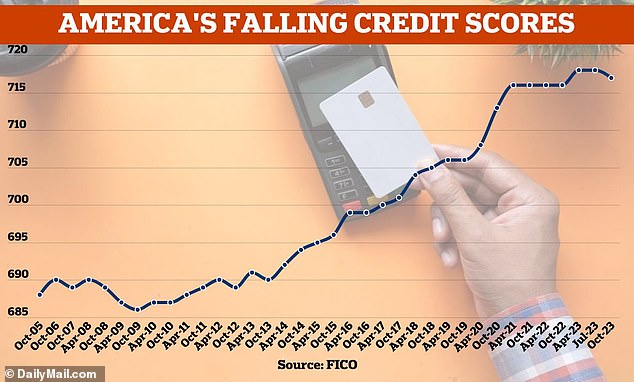

The critical warning emerges as Americans' Credit scores drop for the first time in ten years. thanks to record high prices and elevated interest rates pushing more Americans further into debt.

The nationwide average credit score dropped to 717 from its peak of 718 at the start of the previous year, as reported by FICO.

In the past decade, each time an average score was recorded, it showed either growth or stability—climbing from 690 in October 2013 to 718 last April.

Nevertheless, an additional specialist previously mentioned this last year. busted another big myth , where achieving a solid score is sufficient instead of an impeccable one.

As soon as your credit score reaches 740, you are deemed to have an excellent rating for credit cards, car loans, and various non-mortgage financial products, says Ted Rossman, senior industry analyst. Bankrate .

"For mortgage purposes, I'd set the cutoff at 780," he stated. Pawonation.com .

After that stage, I would certainly keep up with the positive practices that contribute to a solid credit score, yet I wouldn’t stress over achieving flawlessness.

He stated that achieving a higher score doesn't offer any real advantages; instead, it merely gives you something to boast about.

Read more

Post a Comment